Purchasing a home is arguably one of the most significant milestones in life. For aspiring homeowners, the decision to buy or rent can be influenced by financial circumstances, lifestyle, and personal values. For many Muslims, the additional consideration of ensuring financial decisions comply with Shariah law, including the prohibition of riba (interest), can make this choice even more complex.

This educational guide outlines some of the key differences between renting and buying a home, focusing on halal homebuying options – to give you more information on the options available.

Renting: A Flexible, Short-Term Solution

Renting can be an appealing option, particularly for those seeking flexibility or not yet ready for the commitment of homeownership. Here are some key factors you may consider:

Benefits of Renting

Flexibility: Renting generally allows you to move quickly, whether for job opportunities or personal reasons, without the ties that come with homeownership.

Lower Initial Costs: Generally, renting only requires a deposit and the first month’s rent, making it accessible for those without significant savings.

Maintenance is Covered: Property maintenance and repairs often fall under the landlord’s responsibility, easing financial and time demands.

Drawbacks of Renting

No Equity: Rent payments do not contribute toward ownership of the home you are living in.

Potential Rent Hikes: Annual rent increases can make budgeting a challenge.

Limited Security: Leases can be terminated by landlords, leaving tenants without long-term stability.

While renting offers short-term freedom, over the long term, it doesn’t provide the financial security and benefits of owning a home.

Buying a Home: A Long-term Investment

Owning a home can provide stability and encourage long-term financial growth. However, for Muslims seeking riba-free solutions, conventional mortgages present challenges. Fortunately, halal homebuying options can offer a viable alternative.

Why Choose Homeownership?

Building Equity: Monthly payments contribute towards owning an asset that may increase in value over time.

Stability: A home of your own can offer long-term security, freeing you from fluctuating rents or landlord decisions.

Creative Freedom: Whether upgrading or redecorating, homeowners have full control over their property.

However, the upfront costs and commitment of homeownership require careful financial planning.

What is Halal Homebuying?

Halal homebuying enables Muslims to purchase property in a Shariah-compliant manner, avoiding interest and adhering to ethical, transparent financial practices. Instead of interest-based debt, these models focus on co-ownership and shared risk. Usual Features of Halal Homebuying:

Co-Ownership Models (Musharakah): You and the finance provider jointly own the property. Over time, you can choose to gradually gradually purchase the provider’s share until full ownership is achieved. Lease-to-Own Agreements (Ijarah): You lease the property from the provider and have the option to acquire ownership after all payments are made. Transparency: Contracts are clear, with no hidden fees or penalties, ensuring fairness and flexibility throughout the process.

Renting vs Halal Homebuying Comparison

Renting

Halal Homebuying

Lower upfront costs

Requires a larger deposit

Flexible to move locations

Can provides long-term stability

No maintenance responsibilities

Can support wealth building through equity

Does not result in asset ownership

Aligned with Shariah principles

While renting is ideal for short-term needs, halal homebuying provides a long-term pathway to stability and ethical ownership.

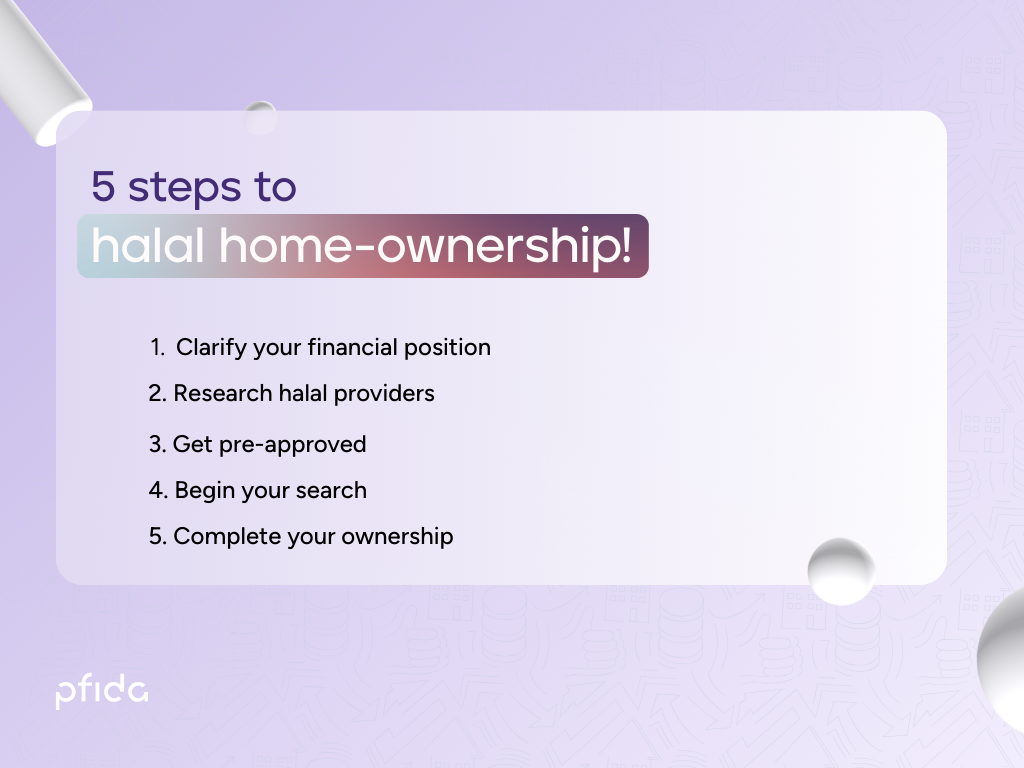

5 Steps to Halal Homeownership

For those ready to explore halal property finance, here’s a guide:

Making the Right Decision

Choosing between renting and purchasing a home isn’t always straightforward, but the decision should reflect your financial circumstances, goals, and beliefs. Renting provides short-term flexibility but may lack the security and financial growth potential of homeownership. Meanwhile, halal homebuying can offer a compelling solution for Muslims seeking to invest in a home ethically and responsibly.

If you’re considering halal homebuying, you don’t have to face the process alone. Reach out to us at hello@pfida.com to get more information.

The content produced by Pfida is intended for general informational and educational purposes only. It should not be construed as legal, tax, investment, financial or other advice. Our products and services do not fall within the scope of financial regulation. This means you do not have any of the protections afforded under the FCA rules and you are not covered by the Financial Ombudsman Service or the Financial Services Compensation Scheme. You should ensure you understand what this means before taking out any of our products or services. If in doubt, you should seek independent financial advice.

Pfida is pleased to announce a strategic partnership with Waafi Bank, a bank that delivers a 100% virtual Islamic banking experience based in Malaysia, aimed at revolutionising the UK Islamic homeownership market.

Under the agreement signed, Pfida will act as an agent for Waafi Bank, enabling the bank to serve its growing customer base of individuals seeking homeownership opportunities in the UK. By leveraging Pfida’s infrastructure, Waafi Bank will be able to offer homeownership solutions and savings accounts more efficiently.

This collaboration marks a significant step in expanding halal homeownership options for UK customers. Rather than developing a new product from scratch, Waafi Bank will utilise Pfida’s proven technology and expertise to enter the market faster and with lower risk.

Raza Ullah, CEO and Founder of Pfida, said, “Our partnership with Waafi Bank supports our mission to increase homeownership opportunities for financially excluded individuals. Muslims are one of the most financially excluded groups in the UK due to the prohibition on interest in the Islamic faith, which limits their access to many financial products.”

He continued, “Our interest-free Home Provision Scheme helps address this issue, and we hope to see more players entering the market to offer similar services. Working with Waafi Bank ensures more people can access Musyarakah-based homebuying opportunities aligned with their faith.”

Waafi Bank’s contribution to the partnership allows Pfida to focus on meeting the growing demand for Sharia-compliant homeownership in the UK, providing ethical and equity-based solutions to thousands of homebuyers.

Dr. Ashraf Iqbal, Chairman of Waafi Bank, said “Pfida is pioneering a new approach to Home Ownership which is in tune with how income stability has evolved within a backdrop of continued economic turbulence. The notion of secure employment, around which the traditional mortgage catered to, has given way to precarious employment, to which this new approach to home ownership is timely. Pfida’s proposition is a much fairer and equitable proposition designed to keep people in their homes when times are bad while increasing their net worths when times are good.”

He continued “I believe Pfida today is similar to Dyson in 1983, when they launched the first ever bagless vacuum. Recall the skepticism and cynicism. Today, bagless is the standard and in time Pfida’s model will be the standard for home ownership.” For more information, please contact: hello@pfida.com; customer@waafibank.com

Pfida has become a notable name in ethical finance, providing innovative, Shariah-compliant solutions to customers across the UK. Whether you’re interested in debt-free homeownership, ethical savings accounts, or simply learning about what Pfida stands for, this article addresses key topics people frequently search for about the company.

What Is Pfida?

Pfida is an ethical financial provider specialising in Shariah-compliant products. Our offerings focus on transparency and community impact, appealing to people looking for alternatives to traditional finance. Key products include interest-free savings options and home financing designed without debt.

What is Pfida’s contact number?

While Pfida doesn’t currently offer phone support, you can reach us easily through live chat, social media, or by emailing hello@pfida.com. We aim to respond to all enquiries within 48 hours.

How long is the waiting list to buy a house with Pfida?

The current estimated waiting time to purchase a home through Pfida’s public waiting list is approximately 5 years. This timeframe applies to applicants who have not invested in a GYS Home account.

Is Pfida Trustworthy?

Pfida has earned trust through our transparent practices and ethical reputation. It is endorsed by organisations such as Islamic Finance Guru and the Islamic Council of Europe. Customer reviews highlight our honest processes and approachable service, further reinforcing our credibility.

How does Pfida make money?

Pfida earns income through rental payments from the home financing model and carefully structured profit margins in our investment products. Rather than charging interest or hidden fees, Pfida’s profit come from transparent and Shariah-compliant agreements that ensure fairness for both the company and our customers.

Can I buy a home with Pfida if I have a low deposit?

You can purchase a home with Pfida, message us at hello@pfida.com or check our product offering at pfida.com for further information.

Why hasn’t Pfida responded to me?

We aim to get back to everyone within 48 hours, but we’ve recently had some delays due to high demand and team changes. As a growing startup (without phone lines just yet), we’re working on upgrading our systems and hiring more team members. Thanks so much for bearing with us, we really appreciate your patience!

Can Pfida’s Services Be Accessed Nationwide?

Yes, Pfida operates across the UK (excluding Northern Ireland) through our seamless, digital-first approach. While the company is based in London, our services are accessible to customers nationwide, ensuring that faith-aligned finance options are available to all.

Is Pfida halal?

Pfida is transforming how faith-aligned finance is perceived and accessed. We’re proud to say our products have been reviewed and certified by Sheikh Haitham Al-Haddad and the Islamic Council of Europe, including our interest-free home financing and savings accounts, which reflect a deep commitment to fairness and transparency. No matter your faith or financial goals, Pfida offers solutions designed to meet modern needs without compromising on values making it 100% halal.

No, Pfida is open to everyone, regardless of faith. While our products are based on Islamic finance principles (such as avoiding interest and promoting ethical investment), they appeal to anyone seeking fair, transparent, and values-driven finance – Muslim or not.

At Pfida, we categorise eligible investors into three key groups to ensure everyone understands the potential risks and benefits of their investment. Here’s a quick breakdown to help you find where you fit.

Why Do Investor Types Exist?

Investment always comes with some level of risk. Investor categories are designed to ensure that those participating in certain opportunities are qualified or experienced enough to make informed decisions. Pfida’s high standards help protect our clients while offering them access to meaningful opportunities.

The Three Investor Types

1. High-Net-Worth Investor

This category is for individuals with significant financial stability. You qualify if (in the financial year before the date of your investment):

You earned £100,000+ (excluding money drawn from your pension savings)

You held £250,000+ in net assets (excluding your excluding assets such as your primary home and rights of insurance).

These requirements indicate you have the financial footing to confidently explore a diverse range of opportunities, including Pfida’s Grow-Your-Savings account.

2. IFA-Certified Investor

Also known as certified sophisticated investors, this group requires confirmation from an FCA regulated financial advisor. To qualify:

You need a written certificate from an authorised financial advisor confirming your understanding of the risks involved.

You must have signed a statement (within the last 12 months) acknowledging you’re eligible to receive promotions exempt from Financial Services and Markets Act restrictions.

Not certified yet? Speak to a regulated Independent Financial Advisor (IFA). When you register for an account with Pfida and we’d be happy to connect you with trusted experts familiar with Pfida’s offerings.

3. Self-Certified Sophisticated Investor

If you have prior experience in similar investments or professional finance, you may qualify as a self-certified sophisticated investor. You’re eligible if any of the following apply:

You’ve invested in at least two unlisted companies in the past two years.

You’ve been a member of a business angel network or syndicate for at least the last 6 months.

You’ve worked in private equity or SME financing within the last two years.

You’ve been a director of a company with a turnover of £1 million+ within the past two years.

This category is for those who are already well-versed in navigating more complex investments.

Not Sure Which Category You Fit?

If you don’t currently meet the criteria or you’re not sure which category you fall into, don’t worry! Here’s how we can help:

Speak to an advisor: Gain access to a free consultation with an authorised IFA so that that they can assess your situation and help you work toward eligibility.

Contact Pfida’s support team: Our friendly team is here to guide you and connect you with experienced advisors who understand Pfida’s solutions.

What’s Next?

Once you’ve identified your investor type and confirmed eligibility, it’s time to explore the opportunities within the Grow-Your-Savings program. Designed for those seeking smart, Shariah-compliant options, this account can help you grow your wealth efficiently and transparently.

If you still have questions or need tailored advice, connect with us today. With the right guidance, taking the next step toward your financial goals has never been easier. Click this link to sign up and be redirected to the PLC.

The Three-Tier Saving Method: How to Save Money and Achieve Your Financial Goals

The Three-Tier Saving Method is a simple and effective approach to help you focus on what matters most, whether it’s your dream home, a new car, or peace of mind for the future. Balancing day-to-day expenses with bigger financial goals can feel overwhelming, but with the right budgeting tips and a solid financial planning approach, you’ll learn how to save money and take control of your future. At Pfida, we believe saving doesn’t have to be complicated. Let’s break it down and see how you can make every penny count.

Tier 1: Short-Term Savings

Small goals. Big Impact.

Short-term savings are all about preparing for smaller, immediate expenses without breaking the bank. Think of it as your financial safety net for surprises like replacing a home appliance, fixing your car, or treating yourself to a small reward.

Making a start with short-term savings is easy.

These simple steps ensure you’re ready for smaller, unexpected expenses while keeping your bigger financial goals on track.

Tier 2: Mid-Term Savings

Bigger purchases. Thoughtful planning.

Saving for mid-term goals, like a new car or an exciting holiday, takes more time and effort. The key is to plan ahead so you can avoid last-minute stress and enjoy your achievements without financial pressure.

Strategies for Success:

By taking these steps, you’ll build a manageable plan to achieve those big-ticket goals without relying on credit or loans. Find out more about growing your savings today.

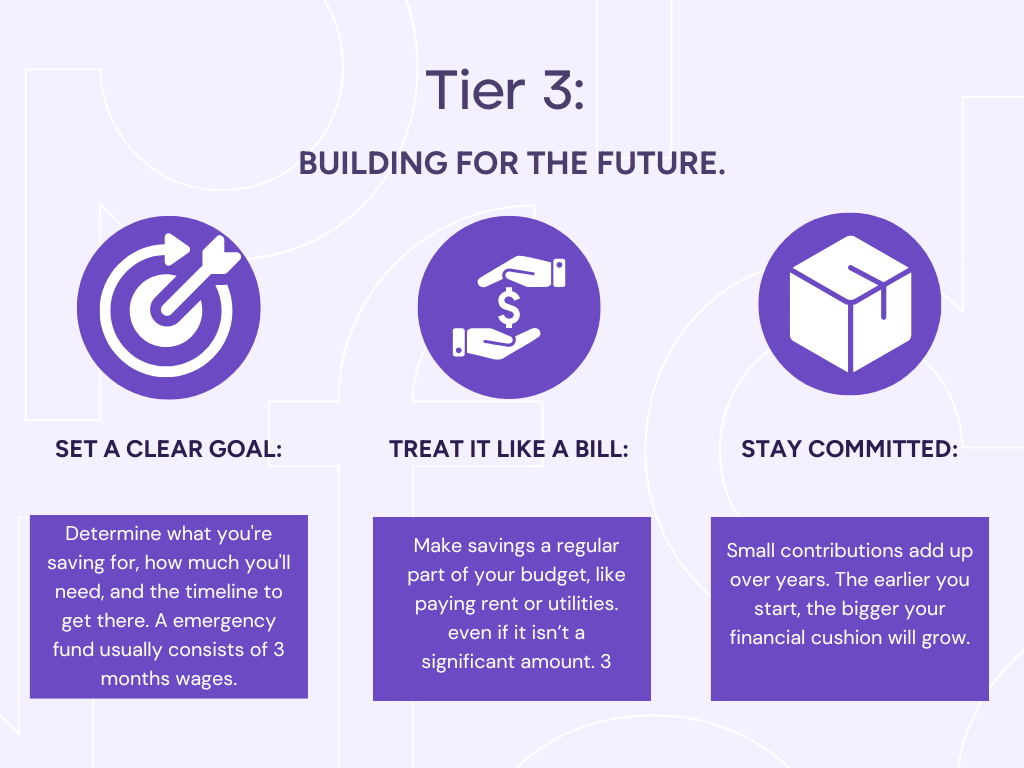

Tier 3: Long-Term Savings

Building for the future.

Long-term savings are about securing your future and achieving life-changing goals, such as buying a home, planning for retirement, or ensuring your children have a solid financial foundation. The secret to success? Start early and stay consistent.

Take Selene, for example. A 35-year-old teacher, she dreamed of owning her own home. By following the three tier model and putting aside £300 every month into a dedicated savings account, she was able to save £21,600 in just six years. She treated her saving contributions like a bill, automating the process to ensure she stayed on track. Now, she’s happily living in her first home, free of financial stress.

Your Long-Term Game Plan:

Contributing regularly, even in small amounts, not only helps you avoid living paycheque to paycheque but also builds habits for financial security. Over time, these savings turn into a powerful tool to achieve your dreams.

Why the Three-Tier Saving Method Works

The beauty of this method is its simplicity. Instead of tackling all your financial goals at once, it divides them into manageable steps based on timelines and priorities. By focusing separately on short-term, mid-term, and long-term goals, you can meet your needs today while also preparing for tomorrow. This structure allows you to feel more confident and in control of your financial future.

Explore your options with Pfida

Whether you’re just starting your savings journey or looking for ways to level up your financial strategy, Pfida is here to help. We offer you the opportunity to get a FREE consultation call with an Independent Financial advisor designed to provide you with tailored guidance and support to become an IFA certified investor with us. Register now to claim.

Ready to take control of your savings? Look at Pfida products today.

Buying your first home is an exciting milestone, but with it comes a whole new world of jargon like Stamp Duty Land Tax (SDLT).

In this article we’ll talk about:

what it is

whether you need to pay it

and how to calculate it

What is Stamp Duty

SDLT is a tax applied when you buy property or land in England. The amount you pay depends on the property price and whether you qualify for any exemptions or reliefs.

How much is Stamp Duty

The government sets thresholds, meaning you only pay SDLT if your property costs above a certain amount. Use the government’s examples to get an accurate figure.

Pfida Model: Buying through a company

For residential properties, from 1 April 2025:

Up to £125,000 – 0%

The next £125,001 to £250,000 – 2%

The next £250,001 to £925,000 – 5%

The next £925,001 to £1.5 million – 10%

The remaining amount (i.e. above £1.5 million) – 12%

If you’re purchasing another property (such as a second home or buy to let), an extra 5% is added to the standard SDLT rates. However, if you sell your main home within 36 months, you might be able to claim a refund.

If you are buying your property through a company, even if its the only property the company will own, an extra 5% is added to the standard SDLT rates

Stamp Duty for Non UK Residents

If you haven’t been in the UK for at least 183 days in the past year, you’re classed as a non UK resident for SDLT purposes. This means you pay an extra 2% on top of the usual rates. Check if you’re eligible for a refund of the surcharge.

What About Leasehold Properties

If you’re buying a leasehold home, SDLT applies to the lease price as well as the total rent over the lease term (if above a certain threshold). From April 2025, SDLT applies to leases with a total rent over £125,000.

How to Calculate Your SDLT

Not sure how much you’ll need to budget? Use the government’s SDLT calculator to get an accurate figure.

Final Thoughts

SDLT might seem complicated, but understanding the basics can help you plan your finances. Since rules vary by region, we recommend visiting the relevant official sites for more details. If you want to see some examples of Stamp Duty calculations for England, check out the official Stamp Duty Land Tax website for accurate and up-to-date information. If you’re purchasing a home in Scotland check out: Land and Buildings Transaction Tax (LBTT) and for Wales: Land Transaction Tax rates and bands | GOV.WALES

Ready to take the next step? Let’s talk!

This article is for information purpose only and shall not be treated as professional advice. When purchasing a property, you should consult a suitably qualified and experienced professional, such as a solicitor or accountant, to seek tax advice.

The content of this promotion has not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000. Reliance on this promotion for the purpose of engaging in any investment activity may expose an individual to a significant risk of losing all of the property or other assets invested.

This website is provided by Pfida Ltd, a company registered in England and Wales with company registration number 10347817 and registered office at 124 City Road, London, England, EC1V 2NX. You can send any requests for further information or queries to info@pfida.com.

Pfida’s products are suitable for IFA-certified, high net worth or self-certified sophisticated investors. By continuing to access this site, you confirm you fall into one of these categories. If you do not, please do not proceed further.

IFA certified (sophisticated) investor

You are an IFA certified (sophisticated) investor if you have:

(a) a current certificate in writing signed by an authorised person confirming that you are sufficiently knowledgeable to understand the risks associated with the description of investment stated in (b) below; and

(b) you have signed, within the last twelve months, a statement in the following terms:

“I make this statement so that I am able to receive promotions which are exempt from the restrictions on financial promotion in the Financial Services and Markets Act 2000. The exemption relates to certified sophisticated investors and I declare that I qualify as such in relation to investments of the following kind: unlisted shares, investments acknowledging the indebtedness of an unlisted company, investments constituting an alternative finance investment bond issued by an unlisted company, and investments conferring entitlement or rights or units in a collective investment scheme, or options to acquire or dispose of an investment, or rights under a contract for the sale of an investment, with respect to investments falling within the categories above. I accept that the contents of promotions and other material that I receive may not have been approved by an authorised person and that their content may not therefore be subject to controls which would apply if the promotion were made or approved by an authorised person. I am aware that it is open to me to seek advice from someone who specialises in advising on this kind of investment.”

High net worth individual

You are a high net worth individual you have completed and signed, within the last twelve months, a statement confirming that in the last financial year:

(a) you had an annual income of £100,000 or more (not including any one-off pension withdrawals) and specifying your income to the nearest £10,000.

(b) You had net assets of £250,000 or more (not including your home or primary residence, any loan secured on it or any equity released from it, your pension (or any pension withdrawals) or any rights under insurance contracts and specifying your net assets to the nearest £100,000.

Self-certified sophisticated investor

You are a self-certified sophisticated investor if you have completed and signed within the last twelve months a statement confirming that you have:

(a) made two or more investments in an unlisted company in the last two years and specifying how many such investments you have made. (This includes any investment made in Pfida Finance Plc); or

(b) worked in a professional capacity in the private equity sector, or in the provision of finance for small and medium enterprises in the last two years and specifying the name of the business/organisation; or

(c) been a director of a company with an annual turnover of at least £1 million in the last two years and specifying the name of the company and its Companies House number (or international equivalent); or

(d) been a member of a network or syndicate of business angels for more than six months and are still a member and specifying the name of the network or syndicate.

For each of the above categories, your declaration confirmed that you understand that this means:

(a) you can receive financial promotions where the contents may not comply with rules made by the Financial Conduct Authority (FCA); and

(b) you can expect no protection from the FCA, the Financial Ombudsman Service or the Financial Services Compensation Scheme.

You are aware that it is open to you to seek advice from someone who specialises in advising on investments. You accept that you could lose all the money you invest.

This communication is exempt from the general restriction (in section 21 of the Financial Services and Markets Act 2000) on the communication of invitations or inducements to engage in investment activity on the ground that it is made to a high net worth individual or certified sophisticated individual or self-certified sophisticated individual.

The content of this website has not been approved by an authorised person within the meaning of the Financial Services and Markets Act 2000.

Reliance on this website for the purpose of engaging in any investment activity may expose an individual to a significant risk of losing all of the property or other assets invested or of incurring additional liability.

If you are in any doubt about the investment to which the communication relates, you should consult an authorised person specialising in advising on investments of this kind.